Soft declines are the most recoverable kind of payment failure in subscription billing, and also the easiest to mishandle. A card that is temporarily out of funds gets treated the same as a stolen one: retried on the same generic schedule, with no adjustment for why the payment failed or what would actually change the outcome.

This guide covers how to separate soft declines from hard ones, diagnose the real cause of each failure, fix what is suppressing first-attempt approval, and build retry and outreach logic around the failure type rather than a fixed schedule.

The scale of the problem is easy to underestimate. A Forrester study found involuntary churn, subscribers lost to a failed payment rather than an active decision to leave, accounts for roughly 34% of total churn at the average subscription business, and industry analysts project failed subscription payments will cost businesses roughly $129 billion globally this year. In most of these cases, the customer never actually decided to leave. A card expired, a bank flagged an unfamiliar charge, or a balance was briefly short.

Step 1: Separate soft declines from hard declines

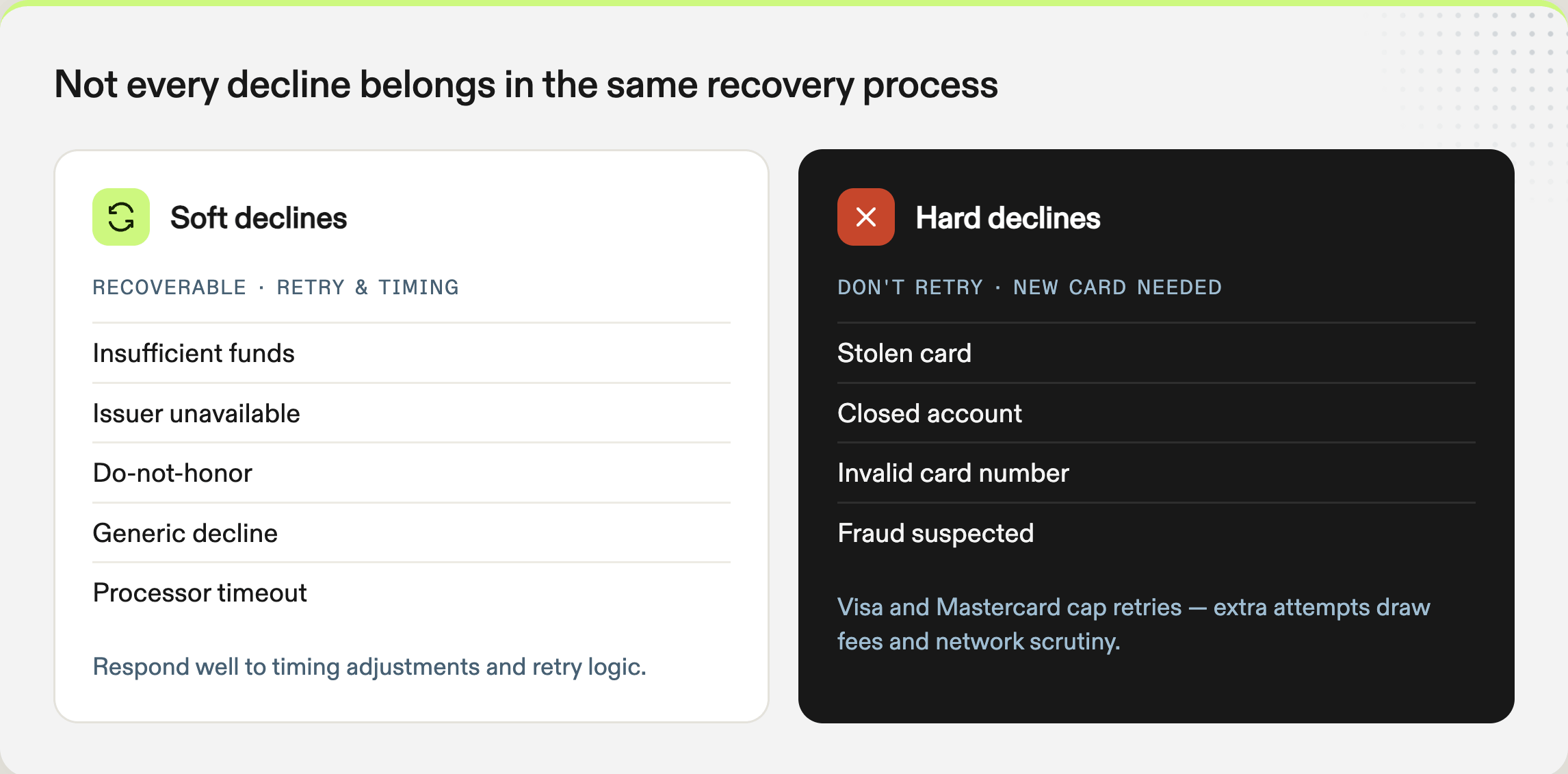

The most useful distinction in payment recovery is also the most frequently ignored. Soft declines require a change to the payment process. Hard declines require a change to the payment method. Treating them the same way wastes retries on failures that cannot succeed and abandons failures that still could.

Soft declines: insufficient funds, issuer unavailable, do-not-honor, generic decline, processor timeout

Hard declines: stolen card, closed account, invalid card number, fraud suspected

Soft declines account for 80% or more of payment failures at most subscription businesses, and four of the five most common decline reasons fall into this recoverable category. They may respond to better retry timing, a different routing path, updated credentials, or more complete transaction data. Hard declines need a new card on file, and retrying them wastes authorization attempts — both Visa and Mastercard cap retries against a single failed transaction, with fees and network scrutiny once those limits are exceeded.

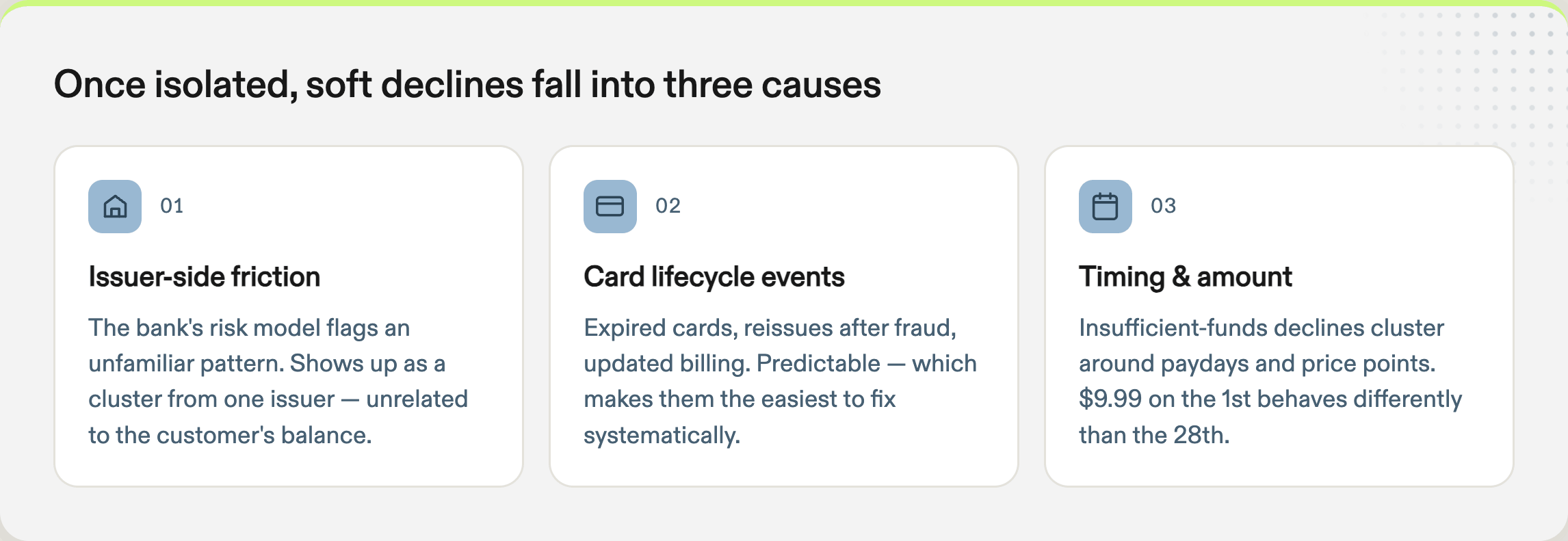

Step 2: Diagnose the root cause

The same decline code can appear across transactions with very different underlying causes. A do-not-honor response may reflect issuer risk, stale credentials, poor timing, or incomplete transaction data. Responding to the code alone applies the same fix to failures that need different ones.

A stronger approach looks for patterns across issuers, processors, card types, billing dates, transaction amounts, and customer tenure before deciding what to do next.

Issuer-side friction shows up as a concentration of declines tied to one issuer or region, often with no connection to the customer's willingness or ability to pay. The fix is usually adjusting how the transaction is formatted or where it is routed. Learn more about why recurring payments get declined even when cards are valid.

Card lifecycle events — expired cards, cards reissued after fraud, outdated stored credentials — are predictable, which makes them the easiest category to address systematically through tokenization and account updater services.

Timing and amount sensitivity drives insufficient-funds declines that cluster around billing dates and pay cycles. The same charge can perform very differently depending on when it is submitted and which customer segment it is hitting.

Renee Harshey, Director of Subscriptions and Retention at Adaptive Health (Healthy Directions), described this at SubSummit this year: once her team separated decline reasons instead of treating them as one churn bucket, recovered payments delivered a 15% lift in retained revenue.

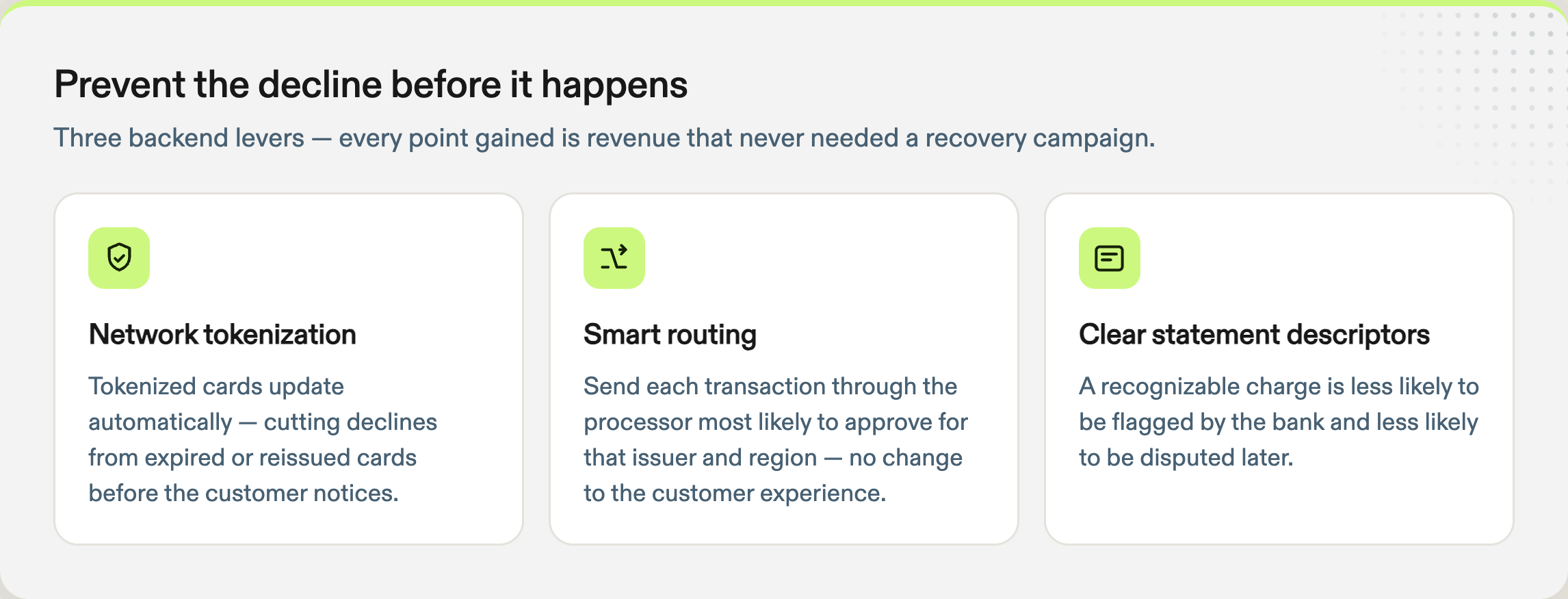

Step 3: Improve first-attempt approval

Every failed payment introduces the possibility of customer friction — a warning notice, an interrupted service, a decision that resolving the problem is not worth the effort. Even when the payment is eventually recovered, the experience has already been disrupted. First-attempt approval removes that risk entirely.

Three factors move first-attempt approval rates most reliably:

Network tokenization replaces stored card numbers with tokens that update as the underlying credentials change. This reduces declines caused by expired or reissued cards, keeps stored credentials current, and gives issuers cleaner authorization data — all without asking the customer to do anything.

Smart routing uses performance differences across issuers, processors, regions, and card types to send each transaction through the path with the strongest likelihood of approval. Small routing improvements create meaningful revenue lift across a high volume of recurring charges.

Clear statement descriptors reduce both declines and disputes. A charge the cardholder recognizes is less likely to be flagged by their bank and less likely to be disputed after it clears.

These are backend fixes with no customer-facing impact, which makes them the highest-leverage place to start. Every payment that clears on the first attempt is revenue that never needed a recovery campaign.

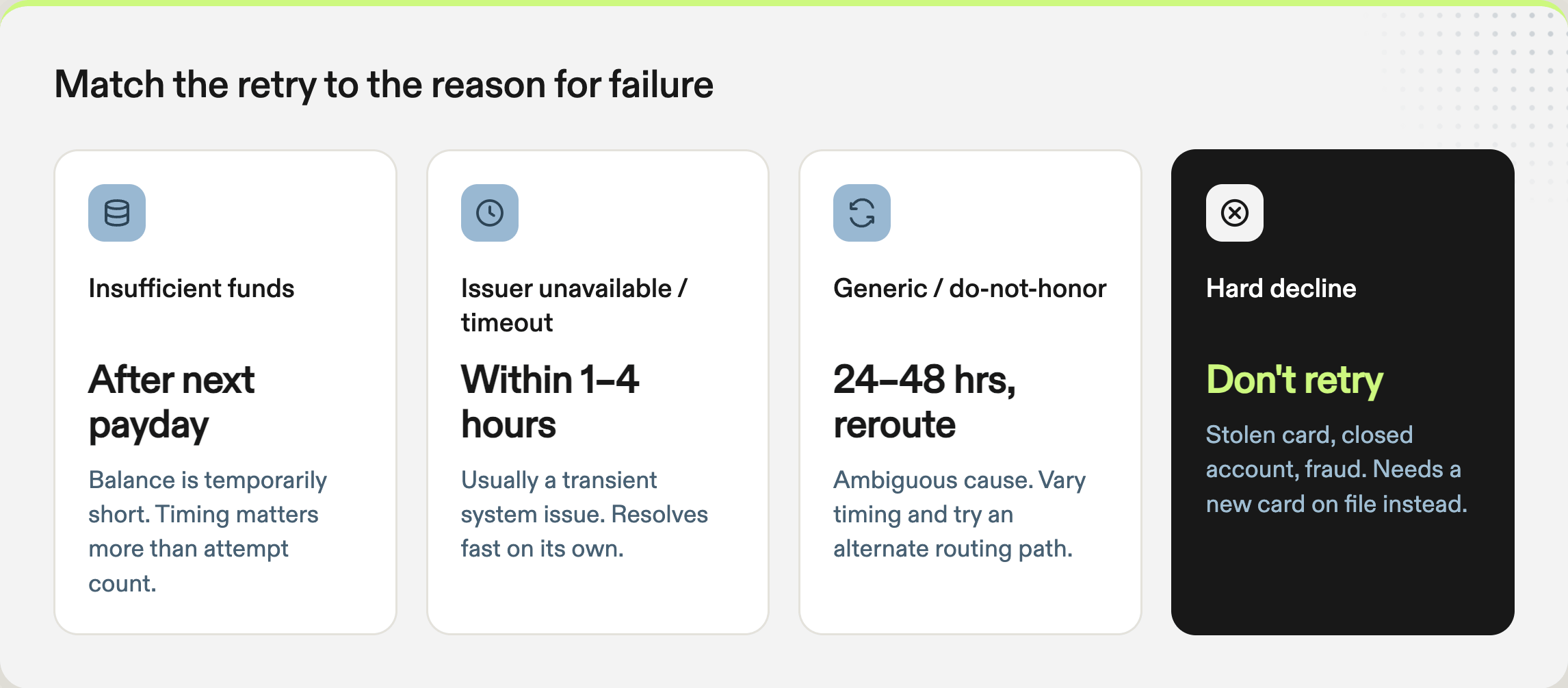

Step 4: Match retry logic to the failure type

A retry is most effective when the next attempt is meaningfully different from the one that failed. Most billing platforms do not do this — they apply the same schedule and process to every failed payment, regardless of why it failed.

The reason matters more than the timing:

Insufficient funds: retry after a likely payday or cash-availability window, not the next day

Issuer unavailable or processor timeout: retry within a few hours, since these issues often resolve quickly

Generic or do-not-honor declines: adjust the transaction data or routing path before retrying — repeating the same request gives the issuer no new reason to approve it

Card lifecycle issues: refresh credentials before the next attempt, since an expired or replaced card will continue to fail on the same stored information

Industry benchmarks show reason-specific retries recovering 45% to 70% of soft declines, well above what a generic fixed schedule typically returns, and because recovered revenue carries no additional acquisition cost, the return on that effort is disproportionately high.

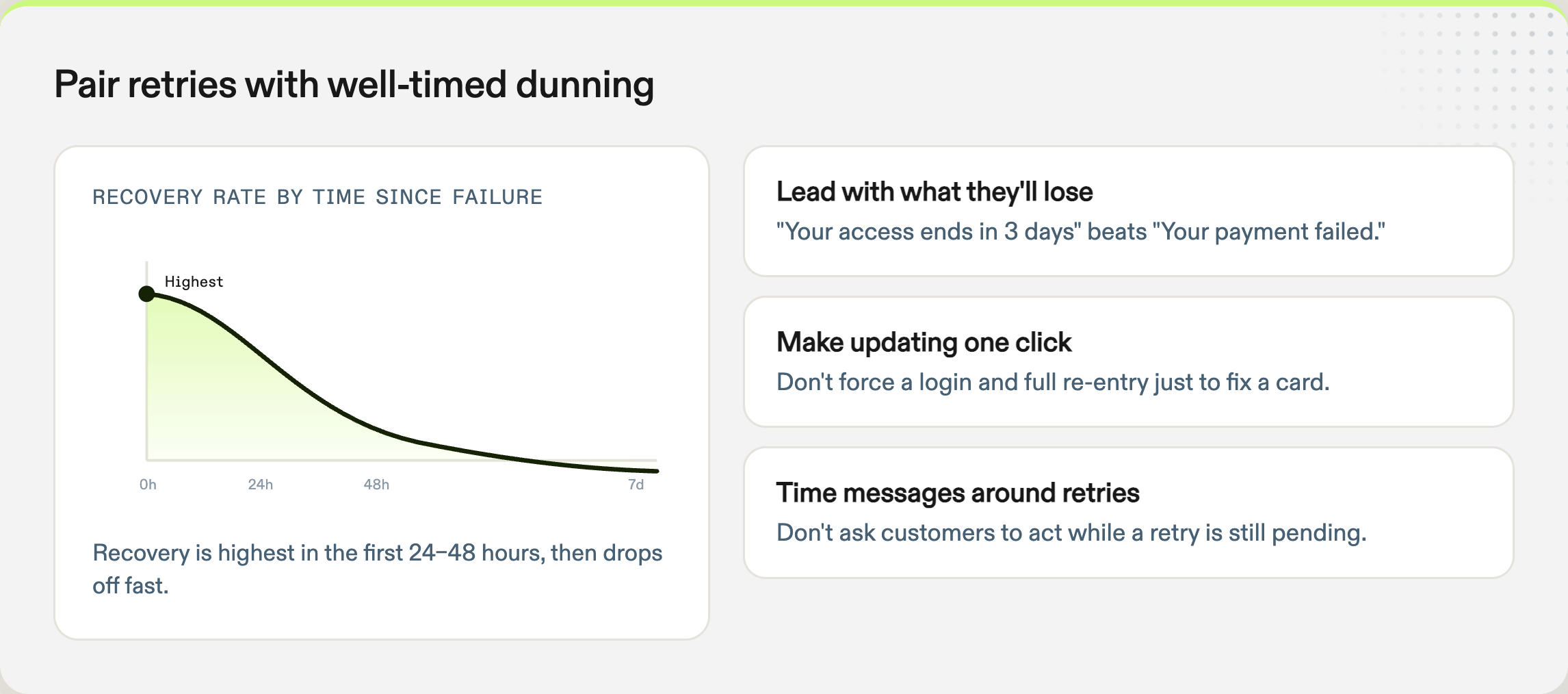

Step 5: Know when the customer needs to act

Many soft declines can still be recovered without customer involvement. An issuer outage resolves on its own. An insufficient-funds failure clears after a better-timed retry. Outdated credentials refresh through tokenization. Contacting the customer before those options are exhausted draws attention to a problem that may already be on its way to resolving.

The decision of when to reach out should follow the failure type. Silent recovery is the right first move when the issue is likely temporary or when another attempt is still pending. Customer outreach is appropriate when the card is closed or invalid, when intelligent retries have been exhausted, or when the account is approaching service interruption.

When outreach is warranted, a few things separate messages that convert from messages that get ignored: leading with what the customer stands to lose rather than the technical failure, making the update process a single step rather than a multi-screen flow, and coordinating the message timing with the retry schedule so customers are not asked to act while a background attempt is still running.

Read more: Preventing Payment Declines — The Revenue Playbook for Subscription Growth

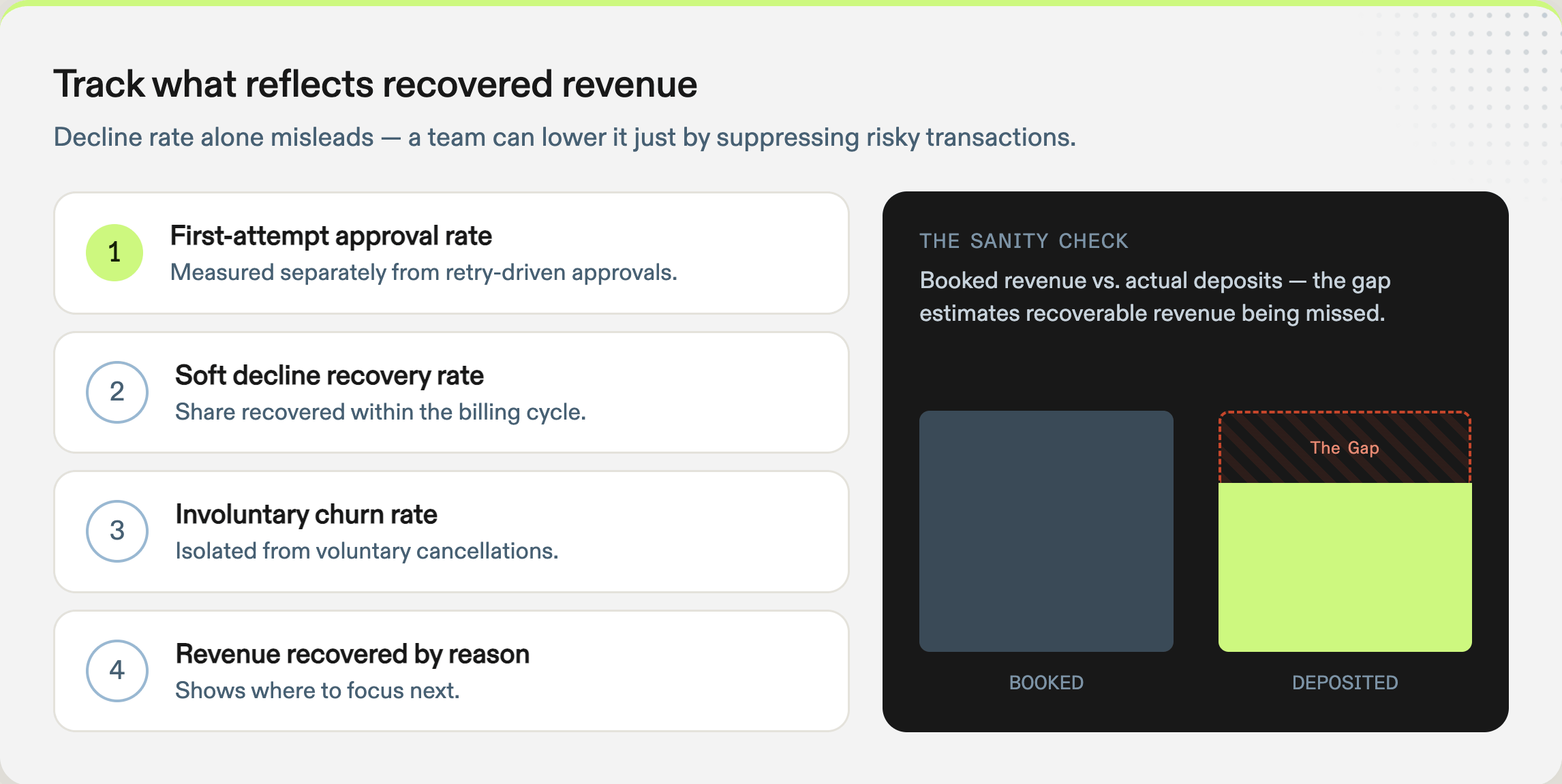

Step 6: Measure recovery accurately

Decline rate alone is a misleading proxy for payment health. A team can lower it by suppressing risky transactions before they are attempted, which improves the metric while quietly reducing revenue.

Better metrics to track:

First-attempt approval rate, measured separately from retry-driven approvals

Soft decline recovery rate, segmented by decline reason, issuer, and recovery method

Involuntary churn rate, isolated from voluntary cancellations

Revenue recovered by decline reason, to identify where the next improvement should come from

Percentage of at-risk accounts retained, which shows whether the customer relationship continued, not just whether the transaction was saved

Customer-assisted recovery rate, which signals whether too many failures are reaching the customer before silent recovery has been fully exhausted

A useful sanity check: compare booked revenue to actual bank deposits over a few recent months. The size of that gap is a rough measure of how much expected revenue is disappearing between billing and settlement.

Why this often goes unaddressed

Billing owns the retry logic. Fraud owns the risk rules. Retention owns the churn number. Finance sees the revenue gap. Support handles the complaints. Each team owns part of the process, and the full payment journey often has no single owner, which means the patterns connecting issuer behavior, credential quality, routing, timing, and customer outreach go unnoticed across team boundaries.

It is also not particularly visible work. A recovery-rate improvement does not show up the way a growth metric does, so it tends to wait behind problems that are easier to point to.

Putting it together

Recovering soft declines effectively comes down to a sequence: separate what is recoverable from what is not, diagnose the specific cause of each failure, improve what is suppressing first-attempt approval, apply retry logic that fits the failure type, and reach out to customers only when their action is actually required.

Subscription businesses that run this as one connected process, rather than five separate teams each owning a fragment of it, recover more revenue and lose fewer customers to a problem that was never really about whether they wanted to stay.

Revaly helps subscription and recurring-revenue businesses maximize payment approvals and reduce involuntary churn through behavioral science and machine learning-driven retry guidance.