What's actually happening when a valid card gets declined

When most people hear "payment declined," they picture an expired card or an empty bank account, but the majority of recurring payment failures don't fit that profile at all. They're soft declines: temporary, often recoverable failures where the card and account are perfectly fine, and the payment simply didn't go through this time for reasons that have nothing to do with the customer's intent or ability to pay. The causes are varied, often invisible to the merchant, and almost always addressable with the right approach.

Issuer-side risk filters are one of the most common culprits. Banks run their own fraud and risk models on every transaction, and a recurring charge that looks slightly different from the expected pattern can trigger a soft decline even when the card is valid and the funds are available. A new amount after a plan change, a charge at an unusual time of day, a billing descriptor the issuer's system doesn't immediately recognize. The customer never knows it happened, and neither does anyone on your team unless they're looking at decline codes at the transaction level.

Temporary holds and timing mismatches account for another significant slice of valid-card declines. A customer may have the funds to cover the charge, but a pending hold from another transaction is temporarily reducing their available balance below the authorization threshold. Retry that same charge 48 hours later and it clears without issue; retry it 10 minutes later and it fails again, often with the same unhelpful decline code.

Network-level throttling adds a layer that most subscription businesses never see. Card networks and issuers can throttle authorization attempts during high-volume periods, which means your 2 AM batch of recurring charges is competing with every other subscription business that also thought off-peak hours were the optimal time to run billing, creating a bottleneck that produces declines unrelated to any individual customer's account status.

Processor-issuer miscommunication rounds out the picture. Decline codes are notoriously imprecise, and the most common code in the industry tells you almost nothing about what actually happened. It could mean insufficient funds, a risk flag, a velocity limit, or half a dozen other things, and your system sees the same generic code for all of them, treating each case identically when the correct response for each is fundamentally different.

None of these are customer problems. They're infrastructure problems. And in a subscription model, where the same customer gets charged every billing cycle for the life of their subscription, every one of these failures has the potential to repeat and compound in ways that one-time commerce never experiences.

Why your current stack doesn't catch this

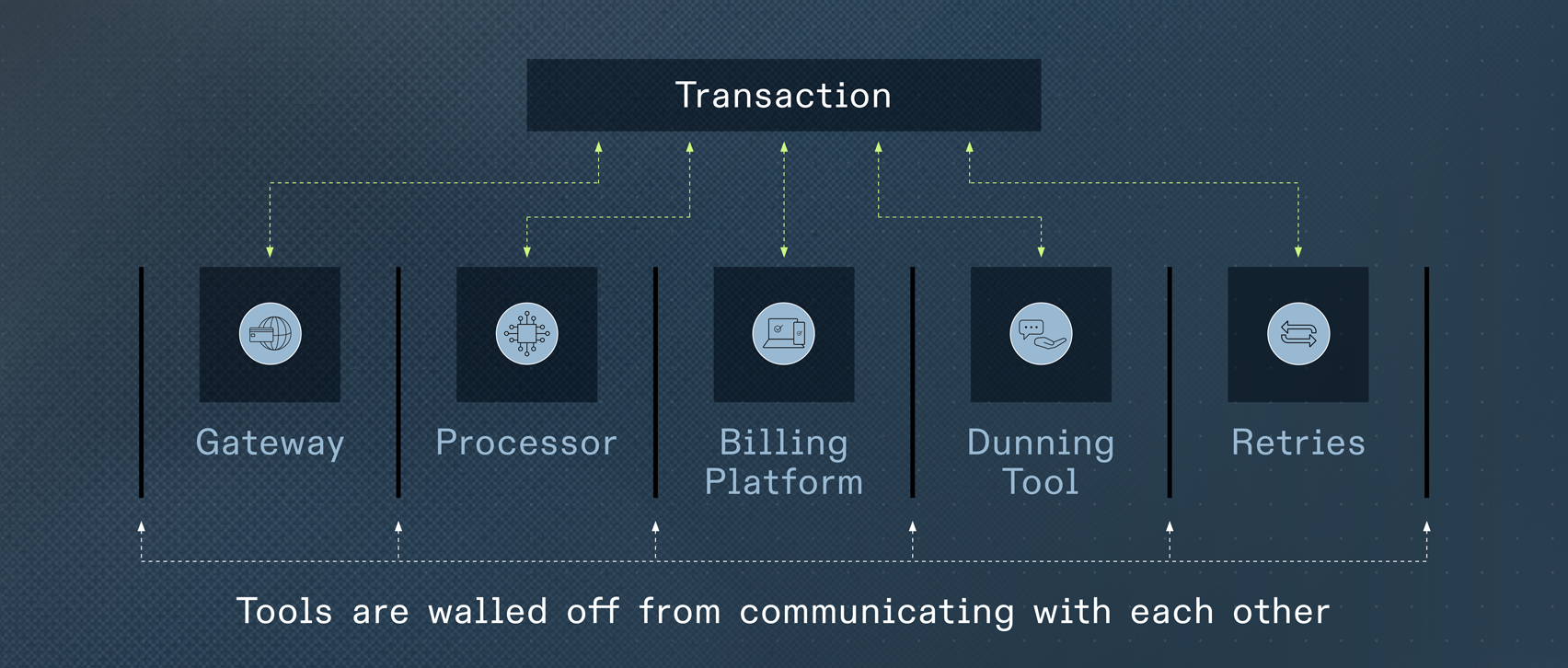

Most subscription businesses didn't set out to build a fragmented payment stack, and nobody made a bad decision along the way. It happened incrementally: you launched with a processor that handled everything you needed, then added a billing platform when plan complexity grew, then bolted on a dunning tool when involuntary churn started showing up in your metrics, and maybe added a retry optimization layer when someone on the team read about smart retries. Each tool solved a real problem in the moment, and each was a reasonable choice in isolation.

The issue is that these tools don't share context with each other, and the gaps between them are exactly where valid-card declines fall through. Your dunning tool doesn't know what your processor knows about issuer behavior patterns. Your retry logic doesn't account for what your billing platform knows about customer payment cycles and plan structures. Your processor doesn't know that this particular charge is the third attempt this week, or that the previous two triggered a velocity flag at the issuer that makes this attempt even less likely to succeed. Each system operates within its own data silo, optimizing for its own narrow view of the problem.

Involuntary churn, churn caused by payment failure rather than a customer's deliberate decision to leave, typically accounts for 20% to 40% of total churn at subscription companies. The majority of it stems from valid cards that could have been recovered with the right approach at the right time.

This fragmentation produces three failure modes. Generic retry logic runs the same fixed schedule for a temporary hold and a closed account, with no way to distinguish between the two. No signal coordination means decline codes, issuer patterns, card network data, and customer history all exist somewhere in your stack but never feed into a single recovery decision. And retry damage, the one most teams miss, means over-retrying a declined card can trigger issuer-level velocity flags that make future authorizations harder, systematically worsening your decline rate over time.

The compounding cost

In one-time commerce, a failed payment is a lost sale. In subscriptions, it's a lost customer along with every future payment they would have made. The industry average failed payment rate runs between 5% and 18% of transactions, and 60% to 70% of those are soft declines on valid cards. A 2% improvement in recovery rate retains those customers for every subsequent billing cycle, and because you already spent the CAC to acquire them, the margin on recovered revenue is effectively 100%.

Every failed payment that converts to a cancellation, when it could have been recovered, is a customer acquisition problem wearing a billing costume.

Four questions to size the problem

1. What is your true failed payment rate, broken down by failure reason? The split between soft and hard declines, with visibility into your top decline codes.

2. What percentage of those failures are on valid, non-expired cards? This defines the recoverable universe.

3. What is your current recovery rate on soft declines? The delta between that and what signal-based systems achieve is your revenue opportunity.

4. Has your effective processing cost per transaction changed in the last 12 months? If your blended rate has drifted up without a clear explanation, rate creep is compounding on top of the recovery gap.

What solving this requires

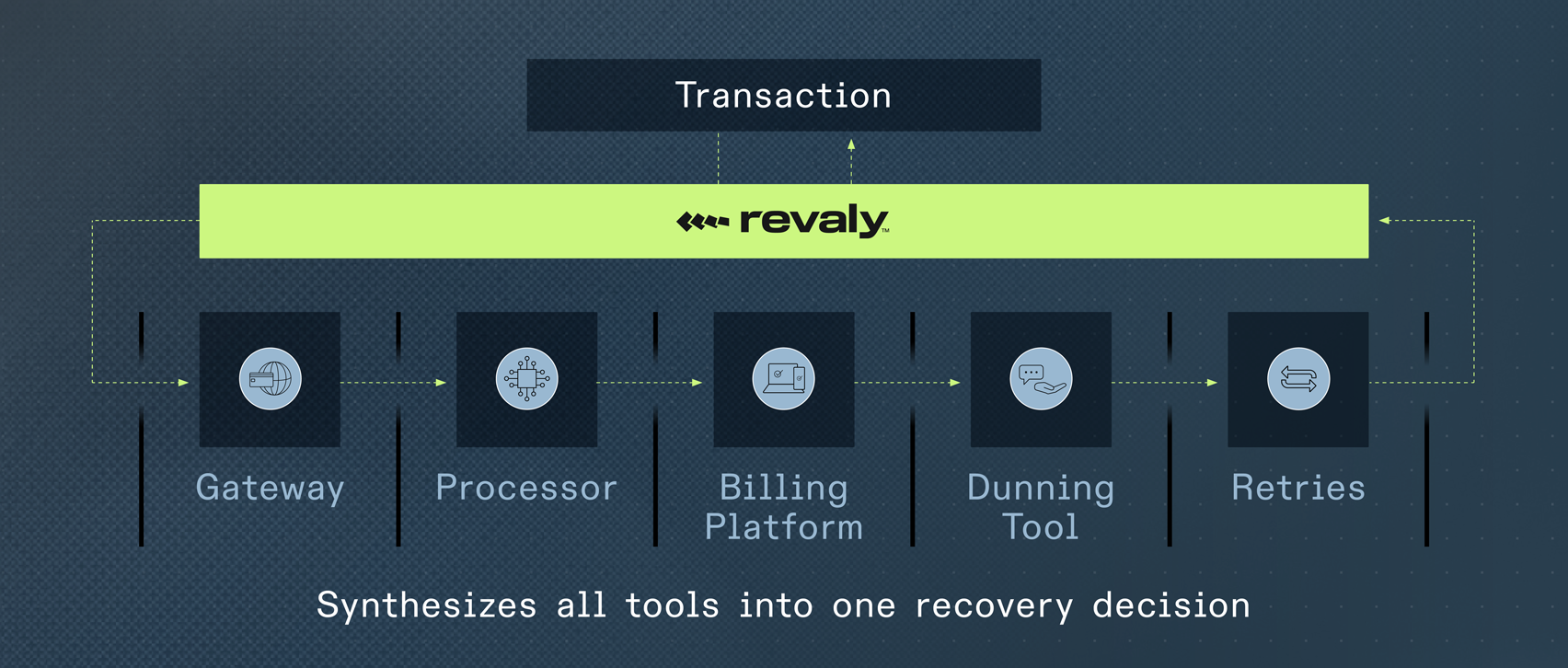

Fixing valid-card declines doesn't mean ripping out your stack. It means adding a layer that sits across it: one that ingests payment events from every processor and billing platform, distinguishes recoverable from terminal in real time, retries based on issuer patterns and customer behavior rather than fixed intervals, and surfaces unified performance data so your finance team can actually answer what the stack is costing you.

Start with the measurement

You don't have to overhaul your payment stack today, but you should know what valid-card declines are costing you, because the number is almost certainly larger than anyone on your team has estimated, and the path from measurement to recovery is more straightforward than most subscription businesses assume.

As the payment landscape grows more complex, with new rails, stablecoins entering the settlement infrastructure, and AI-driven commerce creating new authorization patterns, the businesses with unified, signal-aware payment stacks will be able to adapt faster and capture more of the revenue they've already earned. The ones still running fragmented point solutions will keep paying an invisible tax on every billing cycle, losing customers to a problem that was solvable all along.

The four questions above take an afternoon, and the opportunity is in the answers.

Ready to find out what valid-card declines are actually costing your business? Contact us to start the conversation.