Every subscription business has a failed payment problem. It’s not a question of if you’re going to have the problem — it’s a question of how much it’s costing you and what you’re doing about it.

For most companies, the answer has been some version of the same playbook: retry the charge, email the customer, hope they update their card. This is failed payment recovery, and it’s become an entire category of tools and tactics designed to recapture revenue after a transaction has already been declined.

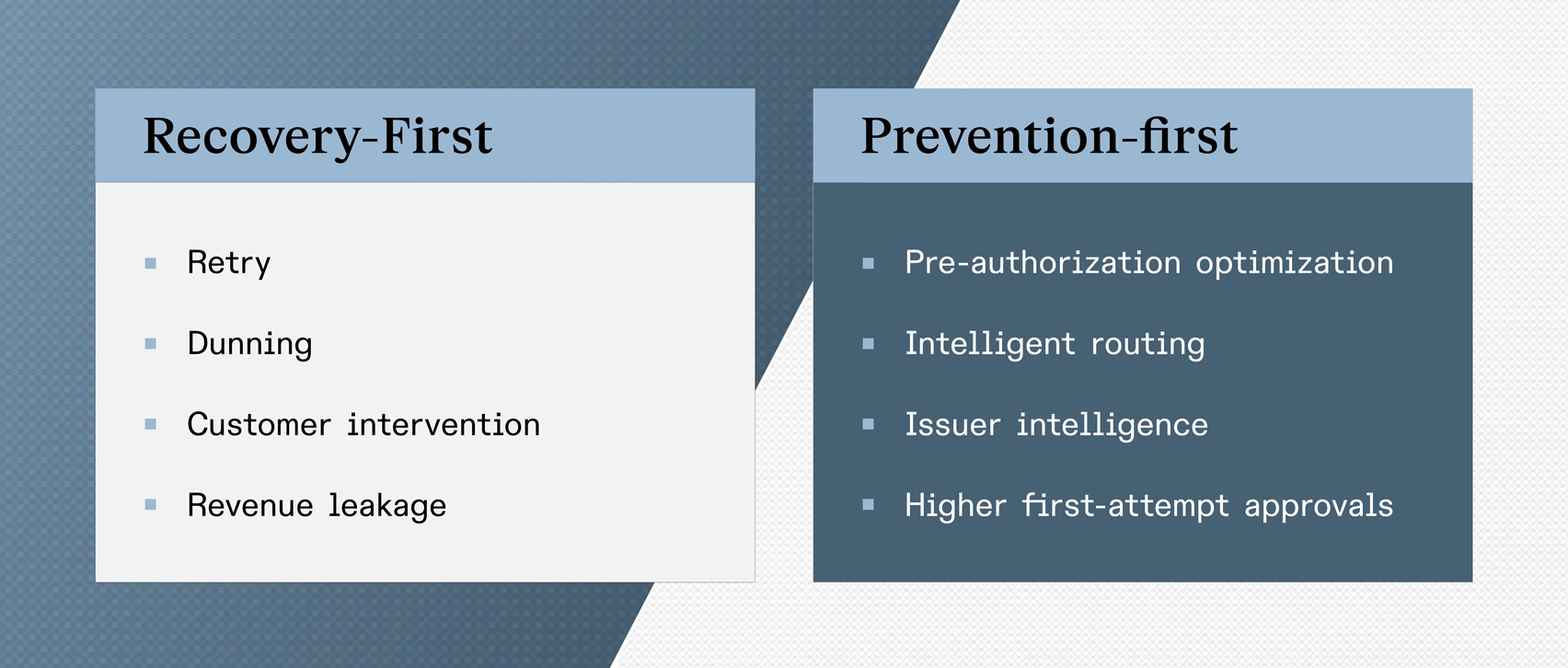

The problem? Recovery is inherently reactive. It accepts payment failure as inevitable and focuses on cleaning up the damage. And while a good recovery process is absolutely necessary, it has a ceiling — one that even the most optimized retry strategies and dunning sequences can’t breakthrough.

Industry data suggests that 5 to 18% of recurring card payments fail, with an average around 13%. According to a Forrester study, involuntary churn — the loss of customers who didn’t choose to leave — accounts for a substantial 34% of the overall churn rate. These aren’t customers who are unhappy with your product. They’re customers whose legitimate payments simply didn’t go through.

This guide covers everything you need to know about failed payment recovery — how it works, what the standard playbook looks like, and why the most advanced subscription businesses are moving beyond recovery toward a prevention-first approach that addresses payment failure at its root.

What is Failed Payment Recovery?

Failed payment recovery is the process of recapturing revenue from recurring transactions that were declined by the customer’s bank or payment processor. It’s a core operational function for any business that relies on subscription billing, membership renewals, or recurring charges.

When a payment fails, the business has a limited window to resolve the issue before the customer’s subscription is cancelled. Recovery typically involves a combination of automated payment retries, customer communication (known as dunning), credential updates, and in some cases, manual outreach from customer support teams.

Recovery is a critical capability. No subscription business should operate without it. But it’s important to understand what recovery actually is: an intervention that happens after a payment has already failed. It doesn’t address why the payment failed in the first place,and it doesn’t reduce the likelihood of the next payment failing. Recovery treats the symptom. It doesn’t treat the disease.

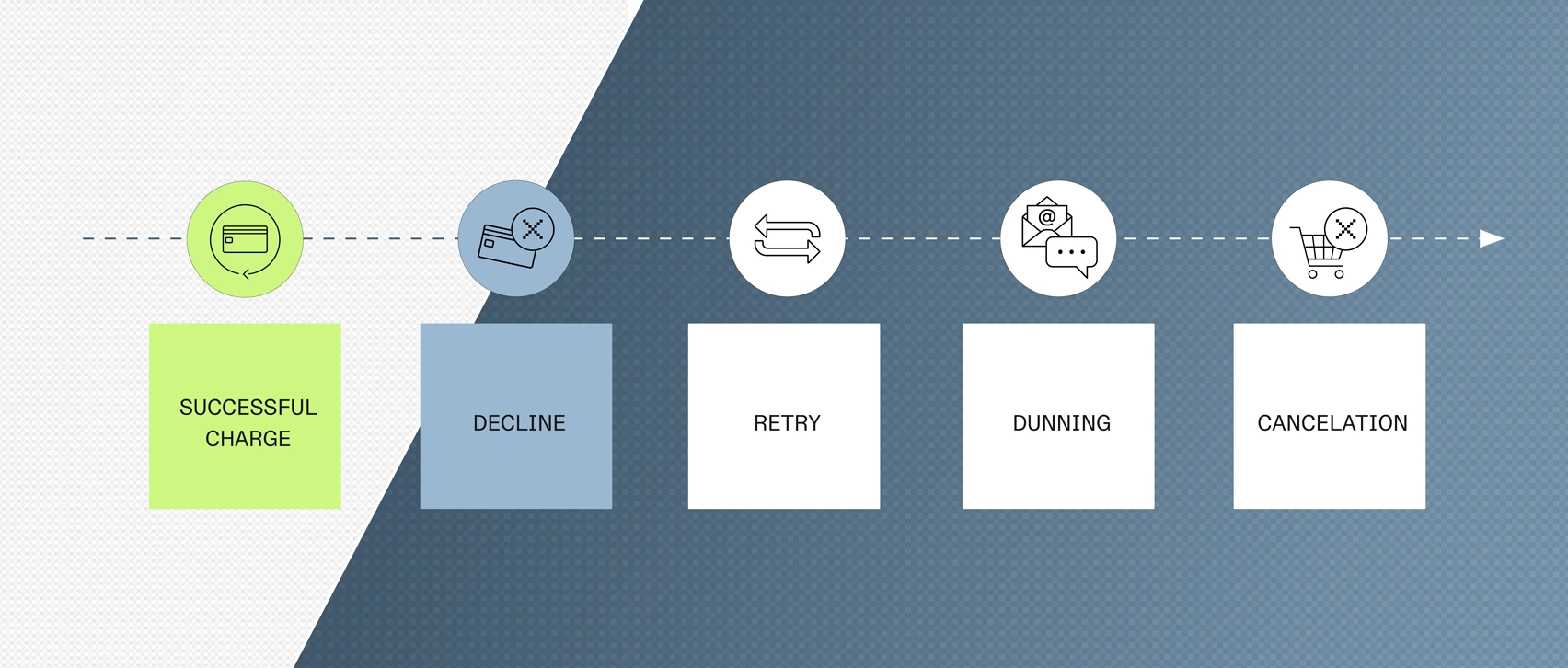

The Failed Payment Lifecycle

The journey from a successful charge to a lost customer follows a predictable chain: a recurring payment is submitted → the transaction is declined by the issuing bank → the business retries the charge → if retries fail, the business contacts the customer → if the customer doesn’t respond, the subscription is cancelled.

Every step to the right of that initial decline is recovery. Everything to the left — optimizing the transaction before it reaches the issuing bank — is prevention. Most subscription businesses invest heavily in the right side. Very few are doing meaningful work on the left.

Why do Payments Fail?

Understanding why payments fail is essential to both recovering them and preventing them. Most recovery tools treat payment failures as a single category, but the reality is far more nuanced — and that nuance matters.

Soft Declines vs. Hard Declines

Soft declines are temporary authorization failures. The card is still valid, but the transaction was rejected for a reason that can often be resolved without customer intervention — insufficient funds, a temporary hold, network issues, or processing errors. Industry data from Checkout.com suggests that the vast majority of payment declines — estimated at 80% or more — are soft declines.Well-timed retries alone can recover 45 to 70% of these transactions.

Hard declines are permanent. The card has been cancelled,reported stolen, or is otherwise unusable. These account for roughly 10 to 20% of declines and cannot be resolved through retries — they require the customer to provide a new payment method.

The problem is that many recovery systems treat all declines the same way: retry a few times, then send a dunning email. Even the best segmentation is still working with information that only becomes available after the payment has already failed.

The Decline Code Problem

When a payment is declined, the issuing bank returns a decline code intended to explain why. In practice, there are hundreds of unique decline codes across different card networks, processors, and issuing banks.Each has its own classification system, and codes are frequently grouped into broad, unhelpful categories. “Do Not Honor,” for example, is one of the most common — and it tells the merchant essentially nothing about the actual reason for the failure.

This opacity makes it nearly impossible for human teams (or simple rule-based systems) to develop optimized responses for every scenario. Each transaction carries dozens of data points, and the combinations create a complexity that brute-force retry logic simply can’t navigate effectively.

The Hidden Causes

Beyond the obvious reasons, there are systemic factors that drive failure rates higher than they need to be — causes that recovery can’t fix because they happen before the decline ever occurs.

Stale or incomplete transaction data. If the data submitted with a payment authorization request is incomplete, incorrectly formatted, or doesn’t match what the issuer expects, the likelihood of a decline increases significantly. This is particularly common in cross-border transactions.

Issuer fraud models flagging legitimate charges. Stripe’s authorization guide notes that authorization rates for online transactions can be 10% or more lower than for in-person payments. J.P. Morgan research puts a finer point on it: as much as 35% of rejected orders turn out to be legitimate, up from 25% year-over-year.

Cross-border friction. According to Solidgate’s analysis, up to 30% of online payments fail due to card declines, fraud checks, and inefficient processing routes. Local acquiring consistently yields higher approval rates.

MID reputation effects. Your Merchant ID carries a history. High decline ratios create a negative feedback loop: more retries lead to more declines, which further degrade your MID health.

Time-of-day patterns. Adyen has found that payments during nighttime hours have approximately a 2% lower success rate. Batch processing that doesn’t account for these patterns leaves revenue on the table.

None of these causes are addressed by dunning emails or customer outreach. They’re authorization-layer issues that require a fundamentally different approach.

The Standard Recovery Playbook

Despite its limitations, a well-executed recovery strategy is essential. Here’s what the current state of the art looks like.

Smart Retries

Basic retry strategies use fixed intervals. Smart retry systems use machine learning to determine the optimal time to reattempt,factoring in the decline reason, the customer’s payment patterns, the issuing bank’s behavior, and broader network trends. A payment that failed due to insufficient funds is more likely to succeed if retried near a common payday.

Dunning Management

When automated retries can’t resolve a failed payment —particularly in hard decline scenarios — dunning sequences become the primary recovery mechanism. Dunning is the process of communicating with customers about their failed payment and guiding them to update their billing information, typically through a series of emails supplemented with SMS orin-app notifications.

Effective dunning segments customers by decline reason,account value, and payment history rather than blasting a one-size-fits-all email. The key principles: communicate early, be specific about the issue, make it easy to update payment information with one-click links, and escalate urgency over time without reading like a collections notice.

Account Updaters and Network Tokens

Account updater services from Visa and Mastercard proactively check stored card credentials against issuing bank records and update them before a payment is attempted. According to Visa, implementing account updater services can reduce card-related involuntary churn by up to 30%.

Network tokens replace card numbers with network-level tokens that persist even when a physical card is replaced. Both tools are valuable but have limitations: account updater success depends on issuer participation, and neither addresses non-credential reasons for failure.

Backup Payment Methods and Customer Self-Service

The last line of defense before cancellation: backup payment method collection at signup, a frictionless payment update page, andextended grace periods that keep the subscription in a “past due” state rather than cancelling outright. Once cancelled, the customer has to re-subscribe rather than simply resuming, which dramatically reduces recovery likelihood.

The Hidden Costs of a Recovery-First Approach

Recovery works. But it also has costs that most businesses don’t fully account for — costs that compound over time.

Revenue Leakage at Scale

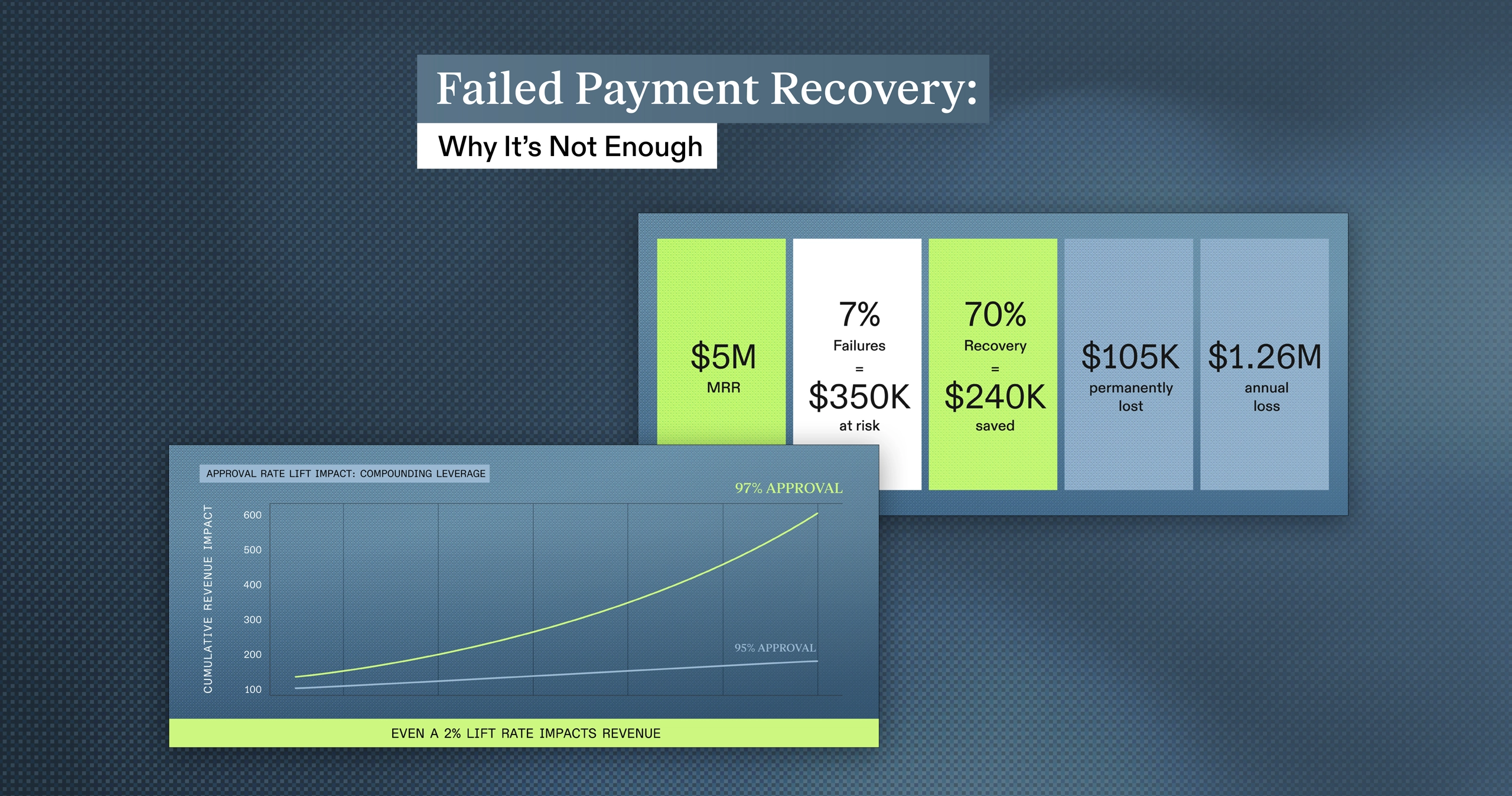

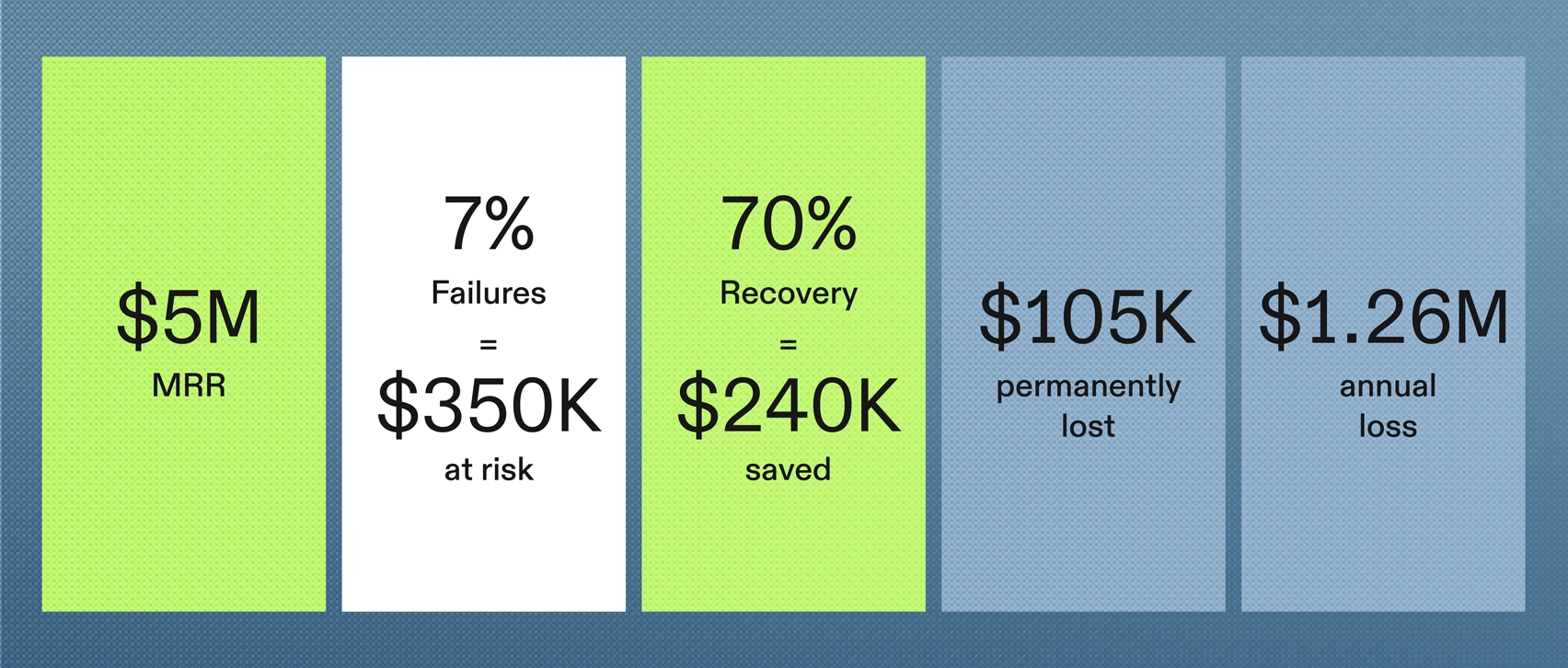

Even at a 70% recovery rate, you’re permanently losing 30% of every failed payment. A subscription business processing $5 million in MRR where 7% of payments fail has $350,000 at risk monthly. A 70% recovery ratesaves $245,000 — but the remaining $105,000 is gone. That’s $1.26 million annually, not counting the full remaining LTV of churned customers.

MID Health Degradation

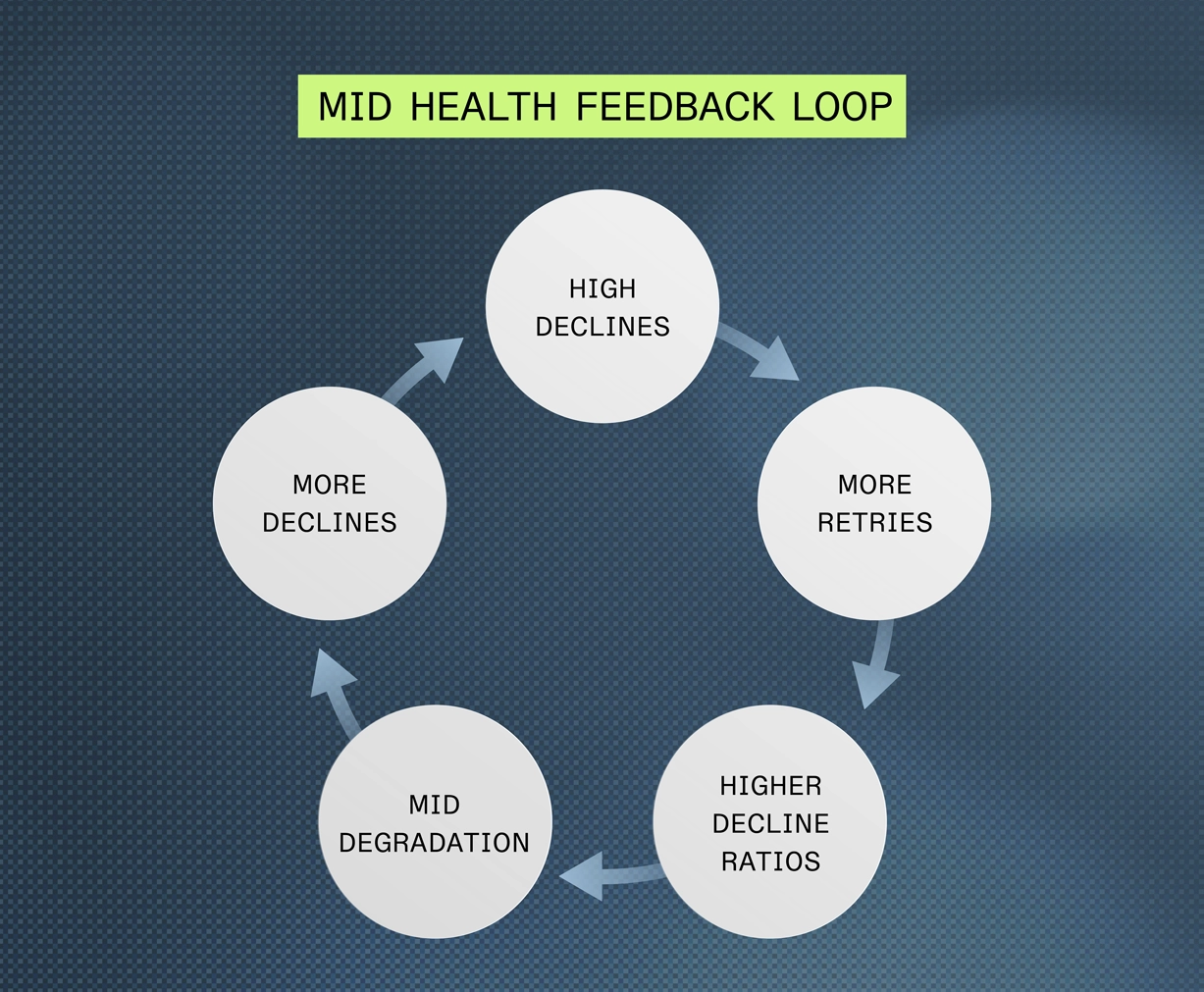

Every failed transaction and retry is recorded. High decline ratios degrade your Merchant ID reputation, leading to higher declinerates on future transactions — creating a vicious cycle. Some processor agreements include explicit decline ratio thresholds and exceeding them can result in increased fees or account termination.

Customer Experience Damage

A recovered payment is not the same as a payment that never failed. ClearSale’s consumer survey found that 41% of customers will never return after a false decline, and 32% will share their frustration on social media. Signifyd’s analysis goes further: Legitimate customers whose orders are declined spend on average 17% to 24% less with the declining merchant after the good order is rejected, and 27% never come back at all.

Operational Overhead

Recovery management becomes a perpetual operational burden distributed across engineering, customer support, marketing, andfinance. It’s a recurring cost that scales with transaction volume without everfully solving the underlying problem.

From Recovery to Prevention: What Approval Rate Optimization Actually Means

Here’s the question that recovery-first strategies don’t ask: what if most of these payments didn’t need to be recovered in the first place?

Approval rate optimization is the practice of maximizing the likelihood that a payment is approved on the first attempt — before it ever becomes a failed payment. Recovery asks, “How do we get this payment through after it was declined?” Approval rate optimization asks, “How do we make sure it’s approved the first time?”

This shift requires working at the authorization layer. The core components:

Pre-authorization data enrichment. Ensuring every transaction is submitted with complete,correctly formatted data that matches what the specific issuer expects.

Intelligent routing. Selecting the optimal acquirer and processing path based on real-time performance data,rather than sending every transaction through a single static connection.

Issuer and network intelligence. Understanding how specific issuers make authorization decisions. The most advanced approaches involve direct issuer relationships enabling bi-directional data sharing.

Continuous learning. ML models analyzing patterns across millions of transactions to identify which BINs, issuers, routing paths, and timing yield the best results.

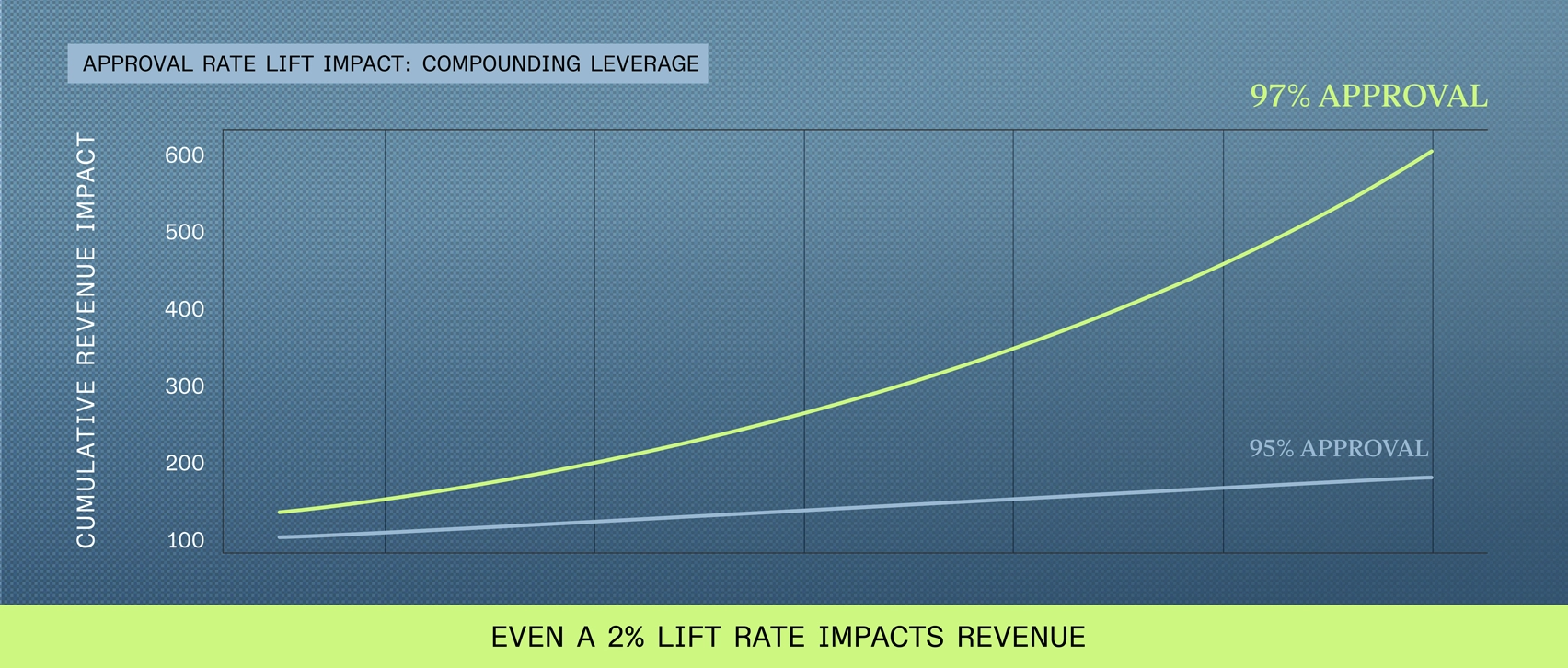

This is the discipline increasingly referred to as Payment Performance Management. As PYMNTS.com recently reported, “in recurring billing, even a 1% to 2% lift in approval rates can materially impact forecasted cash flow and overall forecasted revenue.”

What a Prevention-First Payment Strategy Looks Like

Shifting from recovery to prevention doesn’t mean abandoning your recovery infrastructure. It means layering prevention capabilities on top so that fewer payments fail in the first place.

In a recovery-first model, payments are submitted through a single acquirer connection. When a decline happens, retries and dunning kickin. Typical outcome: 7 to 10% of payments fail, 50 to 70% are recovered, and 2 to 4% of total revenue is permanently lost.

In a prevention-first model, a layer of optimization operates before the payment reaches the issuer. First-attempt approval rates increase, decline volume drops proportionally, and recovery handles a smaller,more targeted set of failures.

These approaches are complementary. Prevention reduces the volume of failures that reach your recovery system. Recovery catches what prevention misses. Together, they create a significantly more effective payment operation than either approach alone.

How to Evaluate Your Current Payment Performance

Most subscription businesses have never audited their payment operations from a prevention perspective. Here are the questions that reveal whether your operation has room to improve:

Do you know your first-attempt approval rate? Not your recovery rate — your approval rate on the initial charge. This is the single most important metric for payment performance.

Are you segmenting declines by root cause? “7% of payments failed” is not actionable. The breakdown by type reveals where the real opportunities are.

What percentage of recovered revenue required customer intervention? If most require dunningand customer outreach, you’re putting the burden on your customers.

Do you have visibility into issuer-level patterns? BIN-level or regional patterns in your decline data are essential for prevention but invisible to most recovery-focused operations.

How many acquirer connections do you use? Single-acquirer setups leave approval rate improvements on the table.

What’s your retry-to-recovery ratio? A high ratio may indicate your retry strategy is too aggressive, contributing to MID health degradation.

Are you measuring the customer experience cost of recovery? Support tickets, reactivation rates, NPS for customers who experienced a failure.

If several of these are blind spots, there’s likely significant revenue being left on the table — revenue that prevention-focused optimization could capture.

Frequently Asked Questions

What is failed payment recovery?

Failed payment recovery is the process of recapturing revenue from recurring transactions that were declined. It typically involves automated payment retries, dunning communications, account updater services,and customer self-service tools.

What percentage of recurring payments fail?

Industry data indicates 7 to 10% of all recurring payments fail, while subscription failure rates range from 5 to 18%, with an average around 13%.

What is the difference between soft declines and hard declines?

Soft declines are temporary failures where the payment method is still valid — estimated at 80%+ of all declines. Hard declines are permanent failures representing 10 to 20% of cases, requiring the customer to provide a new payment method.

How much revenue do subscription businesses lose to failed payments?

According to a Forrester study, involuntary churn accounts for34% of overall churn. GoCardless reports that subscription businesses lose 1 to 4% of customers every month through involuntary churn.

What is approval rate optimization?

The practice of maximizing the likelihood that a payment is approved on the first attempt, by enriching transaction data, optimizing routing, leveraging issuer intelligence, and applying machine learning — all before the payment is submitted.

How does payment performance management differ from dunning?

Dunning communicates with customers after a failure.Payment performance management treats the entire payment lifecycle as an optimization opportunity, focusing on preventing failures before they happen.

Can you prevent failed payments?

Not all — a cancelled card will still decline. But a significant share of declines are caused by controllable factors: incomplete data, suboptimal routing, issuer formatting requirements, and fraud model triggers on legitimate charges.

What impact do false declines have on customer retention?

ClearSale found 41% of customers will never return after a false decline. Signifyd’s data shows loyal customers who return place 65% fewer orders with a 17% lower lifetime value.