Customer acquisition costs across the subscription economy have risen 25–40% over the past two years, depending on the channel. The structural forces driving that shift — platform saturation, the erosion of third-party targeting data, and increasingly competitive auction dynamics on paid social — are not reversing. Most DTC operators understand this. The conversation it has triggered, almost universally, has focused on how to acquire more efficiently.

There is a parallel conversation that has received far less attention. It starts with a number most subscription businesses don't track separately.

Your churn rate is a combined figure — and that matters

When a DTC subscription brand reports its monthly churn rate, that number combines two fundamentally different phenomena. The first is voluntary churn: subscribers who evaluated the product, the price, and the experience, and made an active decision to cancel. The second is involuntary churn: subscribers who were lost because a payment failed and was never recovered. They didn't cancel. They didn't choose to leave. The subscription lapsed, and on the dashboard, they look identical to everyone else who churned.

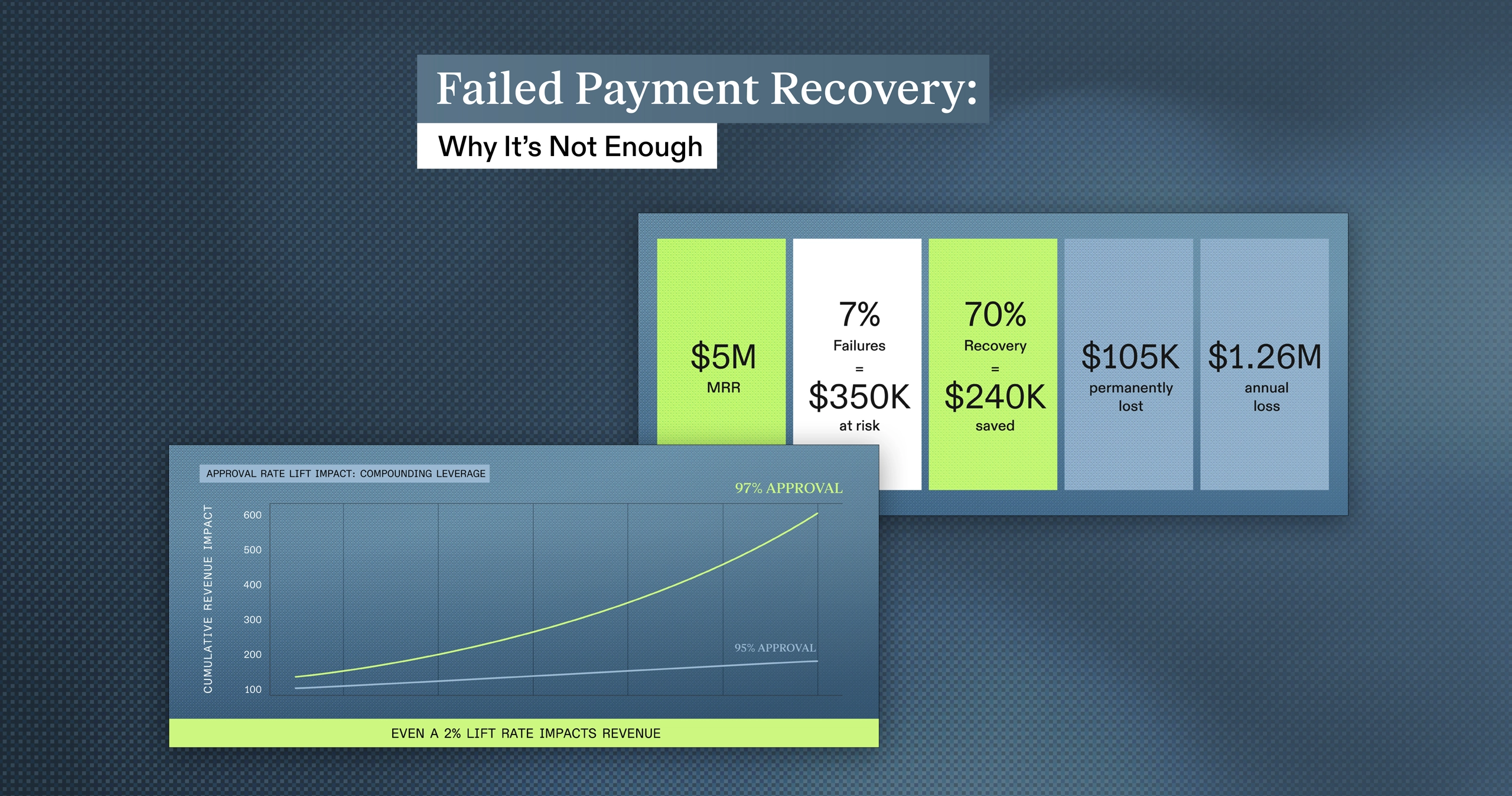

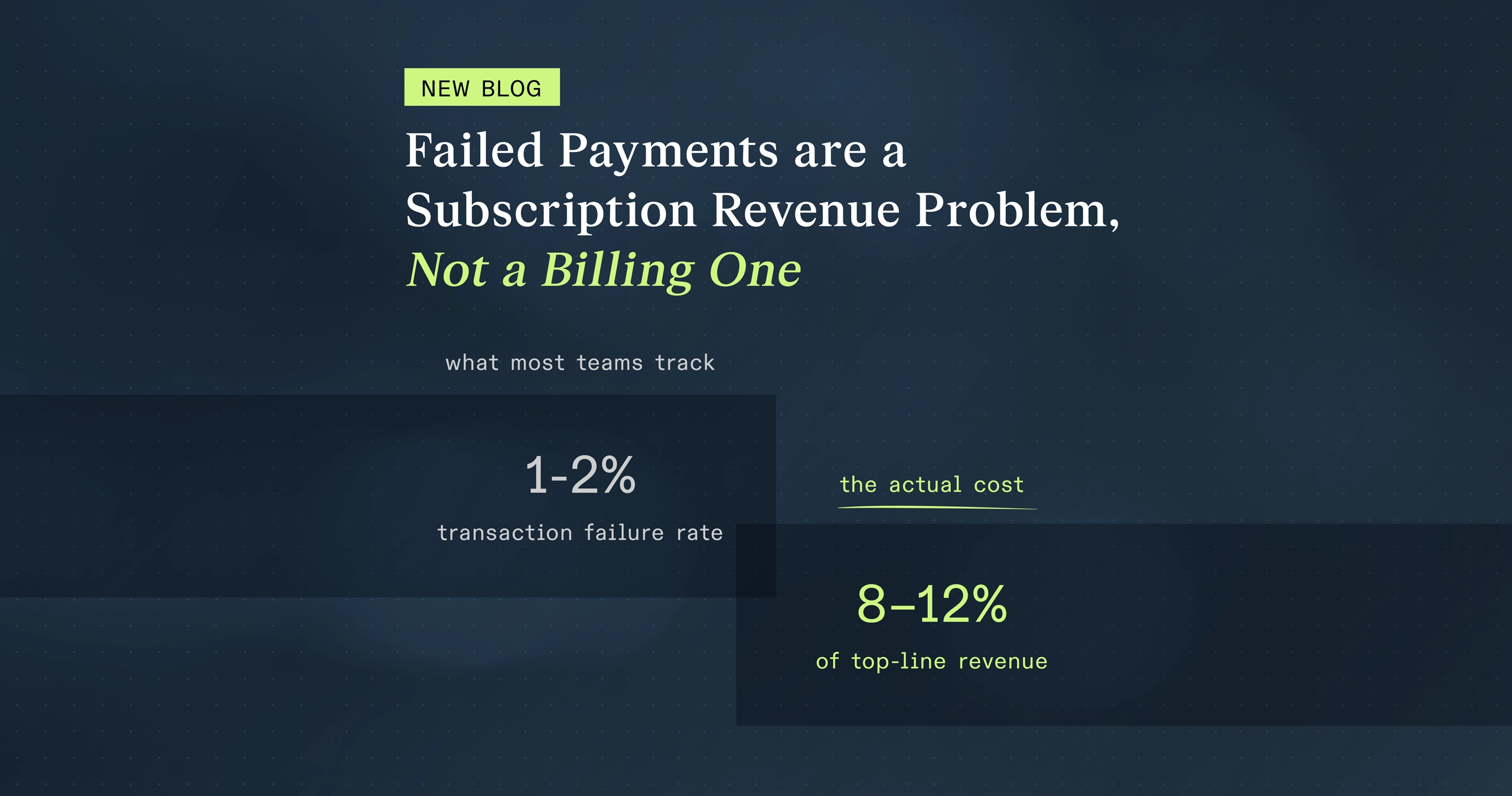

Research from across the subscription industry estimates that involuntary churn accounts for between 20% and 40% of total subscriber loss, depending on the billing model and vertical. In health and wellness specifically, where card-on-file replenishment is the dominant billing pattern, the figure tends to land toward the higher end of that range. A brand with a 5% monthly churn rate may find that 1.5 to 2 percentage points of that number has nothing to do with how customers feel about the product.

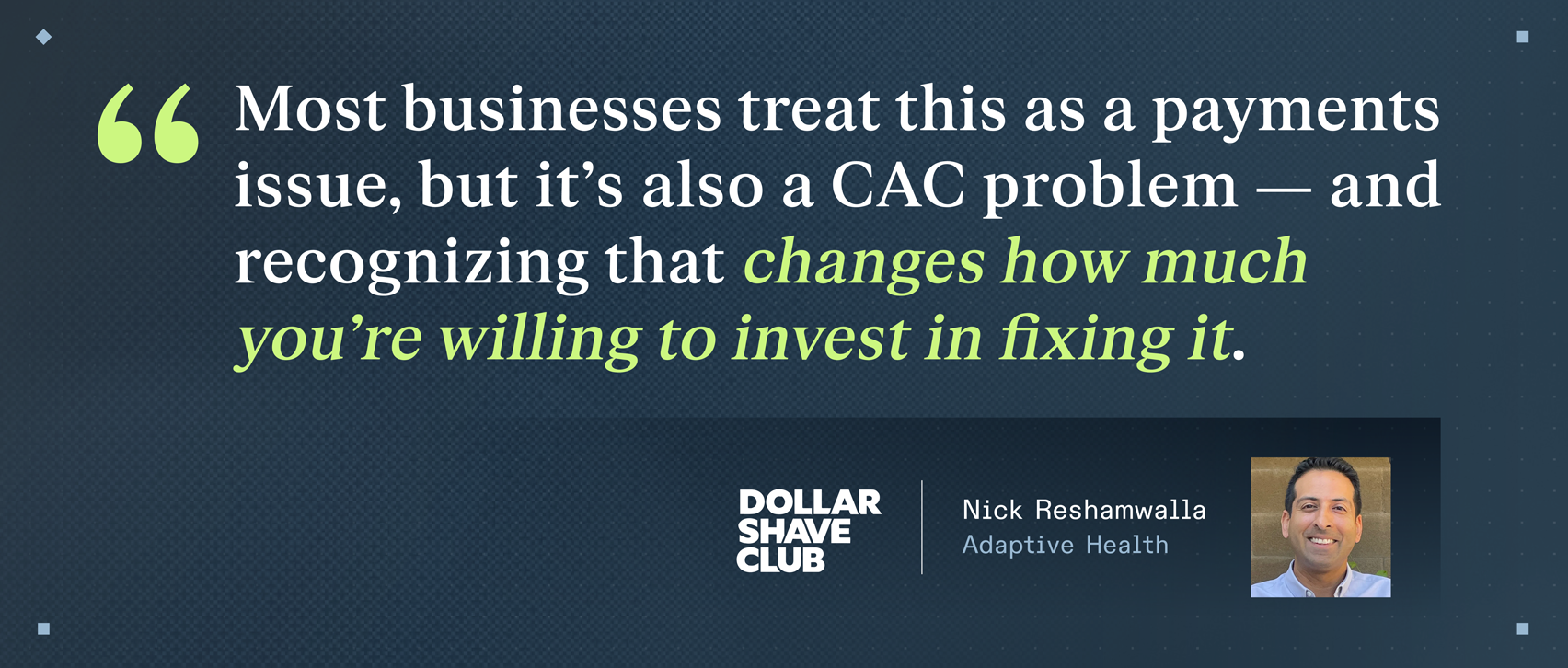

Nick Reshamwalla, who led subscription growth at Dollar Shave Club, put it plainly: "Most businesses treat this as a payments issue, but it's also a CAC problem — and recognizing that changes how much you're willing to invest in fixing it." The distinction between voluntary and involuntary churn is not semantic. Voluntary churn responds to product improvements, onboarding optimization, loyalty programs, and cancel flow interventions. Involuntary churn does not respond to any of those interventions, because the customer was not trying to leave. Applying retention resources to the involuntary portion produces no result and generates misleading signal about what is and isn't working.

Why recurring payments fail more than they should

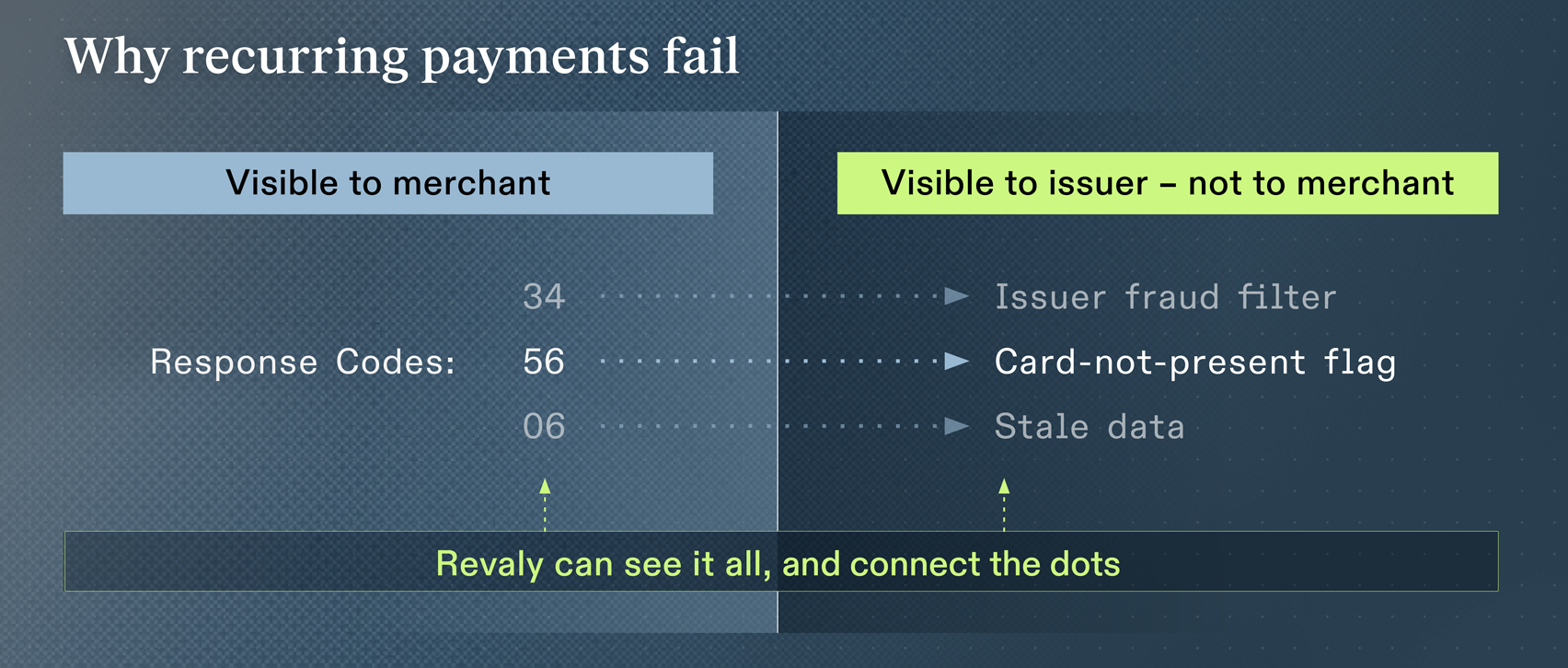

Understanding why involuntary churn happens at the rate it does requires understanding something about how the payment infrastructure was built — and what it was not built for.

Card-not-present recurring billing, the transaction type that powers most DTC subscription businesses, is treated by issuer fraud models as one of the highest-risk transaction categories in existence. This is not because DTC subscription customers are high-risk. The infrastructure was built for one-time card-present transactions. Recurring charges on a stored card, processed without the customer present and often without the customer's active awareness in the moment, fit the behavioral pattern of unauthorized card use closely enough that conservative fraud filters flag them at rates that bear no relationship to actual fraud incidence.

Checkout.com and Oxford Economics, in their 2023 research across four major markets, found $50.7 billion in direct merchant losses attributable to false declines — a 140% increase from their own 2020 estimate for the same markets. The Aite Group's broader global estimate placed the figure at $443 billion for 2020. Global e-commerce has grown by roughly 70% since that estimate was published. For context, global card fraud losses in 2024 were $33.4 billion, per the Nilson Report. False declines are doing more measurable damage than the fraud the industry built its entire defensive architecture to prevent.

At the category level, the picture is more specific. Health and fitness subscription brands lose an estimated 11% of recurring revenue to failed payments annually. For every $1 lost to payment fraud in the subscription economy, approximately $75 is lost to false declines. Most of the involuntary churn a DTC subscription brand experiences is not inevitable. It is a function of infrastructure that was never designed to recognize its customers.

Prevention and recovery are not the same conversation

Most subscription businesses that engage with the failed payment problem start with recovery — the retry logic, the dunning emails, the win-back flows that activate after a decline has already happened. Recovery matters, but it is the more expensive version of the solution. Every recovered payment required a failure first, which means friction for the subscriber, a gap in the billing relationship, and a retry cycle that carries its own failure rate.

The more valuable intervention happens earlier. Payment optimization — formatting transaction requests correctly, using account updater services to keep card data current, timing retry attempts based on issuer behavior rather than fixed schedules, and building cleaner data signals into the authorization request itself — reduces the number of failures that need to be recovered in the first place. A transaction that never fails does not require a recovery sequence and it does not create subscriber friction. And it does not carry the risk that a recovered subscriber, having experienced a lapse in their subscription, decides not to re-engage.

Renee Harshey, Marketing Director of Subscriptions and Retention Programs at Adaptive Health, described the compounding effect of getting both right: once her team addressed both the prevention and recovery layers, they found that approval rates climbed above industry benchmarks for the first time and stayed there. The payment stack was working for them rather than against them.

The brands seeing the most meaningful improvement in involuntary churn are not choosing between prevention and recovery. They are treating them as sequential priorities, with prevention as the foundation.

The CAC multiplier

The cost of involuntary churn has always been material. In the current market, it has become more expensive in a way that compounds.

When a subscriber is lost to a payment failure before their acquisition cost is paid back, the brand has not simply lost a subscriber. It has made a net negative investment. The CAC was spent. The relationship was built. The customer intended to continue. And the subscription lapsed before the economics of the acquisition were resolved.

For most DTC health and wellness brands, the CAC payback period sits somewhere between three and six months, depending on the product and the channel. Acquisition costs are up 25–40% from two years ago. That means the threshold that must be cleared before a subscriber generates net positive value is higher than it has ever been — and the cost of losing a subscriber before that threshold is crossed has risen proportionally.

Renee Harshey's team at Adaptive Health found that recovering one failed payment led to three more payments on average — meaning every recovered subscriber wasn't just a single transaction saved, but a meaningful extension of the customer relationship. "There's nowhere else in our business that you can find opportunities to generate that much revenue," she noted. "This is revenue that we're due." In a market where that relationship took significant acquisition investment to build, the compounding effect of recovery is substantial.

A brand processing $10 million in annual recurring revenue, with a 3% involuntary churn rate and an average CAC payback period of four months, is absorbing losses that don't show up cleanly anywhere in standard retention reporting. They show up as pressure on LTV. They show up as CAC:LTV ratios that don't respond to acquisition optimization. They show up as retention metrics that improve in response to product investment but never quite reach where the model says they should.

What separates brands that address this

The brands that have moved meaningfully on involuntary churn share a few common starting points. They track voluntary and involuntary churn as separate metrics, which requires intentional instrumentation rather than relying on default billing platform reporting. They treat decline codes as diagnostic information rather than binary outcomes, distinguishing between a card that is genuinely unusable and a card that was incorrectly flagged and is likely to succeed on a better-timed, better-formatted retry. And they recognize that retry logic is not a set-and-forget configuration — the intelligence applied to a retry attempt is the primary determinant of whether it succeeds.

Immunotec, the global health and wellness company, found that 31% of their recurring payments were failing before they addressed the problem systematically. Their existing recovery logic was capturing just 6.3% of those failures. Yanick Gianesin, Global Payments and Risk Manager at Immunotec, described their previous setup plainly: "What we had before was as basic as it gets. Three blind retries, and then we just gave up." After implementing intelligent retry infrastructure, recovery rates improved by up to 35% across markets. The payment failures didn't disappear. The infrastructure learned to distinguish between recoverable and unrecoverable declines, and to act on that distinction correctly.

54% of retail declines are recoverable with the right payment intelligence. Most DTC subscription brands are recovering a fraction of that.

The question worth asking

In a market where subscriber acquisition has become more expensive and retention has become more strategically important, the involuntary churn problem deserves more precise attention than most brands are giving it. The subscribers in that segment didn't make a decision. The infrastructure failed them. And in many cases, the right retry at the right moment would have kept them.

Of the subscribers your brand lost last month — how many actually chose to leave? If you're not sure, it's worth finding out. We work with DTC subscription brands to quantify the involuntary churn gap and identify what's actually recoverable. Talk to our team →