When a customer tries to pay you, only two things can happen: the transaction is successful — or it isn’t. And while most teams obsess over acquisition, funnels, and conversion optimization, far fewer ask the question that matters most after the click: Did the payment actually go through?

That question lives inside one deceptively simple metric: transaction success rate.

Transaction success rate measures how often legitimate customers who attempt to pay are actually able to complete the transaction. And while it rarely gets the spotlight, even a one or two point improvement can unlock millions in recovered revenue annually — without increasing traffic, ad spend, or pricing pressure.

Let’s take a deeper look into what transaction success rate means, why payments fail even when they shouldn’t, and how to improve transaction success rates using better data, smarter routing, and issuer-aligned decisioning.

What Does Transaction Success Rate Mean?

Transaction success rate (TSR) measures the percentage of payment attempts that are approved and completed successfully.

If 1,000 customers attempt a payment and 930 go through, your transaction success rate is 93%.

That 7% failure rate represents real customers who wanted to pay you — but couldn’t.

In subscription businesses, the impact compounds quickly: Failed renewals create churn and lost LTV. And some merchant account providers even charge higher fees when transaction success rates are low, using a sliding-scale model for businesses with very poor TSRs. In severe cases, an unusually low transaction success rate can trigger fraud concerns, as it may resemble carding behavior where stolen cards are tested through checkout forms.

Why Payments Fail (Even When They Shouldn’t)

Most declines aren’t fraud, however. They’re system-level decisions triggered by missing data, rigid routing, or conservative issuer logic. When approvals drop, it’s rarely random — it’s the result of signals the issuer is interpreting behind the scenes.

The major failure drivers include:

1. Data Quality & Metadata

Issuers approve what they trust and decline what they don’t.

Common blockers:

- Outdated tokens

- Incorrect billing fields

- Missing metadata

- AVS/CVV mismatches

- Formatting errors across gateways

Why it matters: When a payment record is in complete or formatted poorly, risk engines treat it like a potential threat even if the customer is legitimate.

2. Routing Logic

Most merchants use static or single-path routing. It’s simple but limiting.

Issues occur when:

- A transaction is routed through a suboptimal path

- Domestic payments take an international route

- Retries happen too fast or too often

- Certain BIN ranges perform better on alternative gateways

Why it matters: Routing determines whether a transaction reaches the right issuer in the right format. The smarter the routing, the higher the approvals.

3. Issuer Decision Logic

Issuers run complex risk models that consider:

- Cardholder behavior and history

- Merchant reputation and trust signals

- Velocity patterns (sudden spend spikes)

- Regulatory and network rules

- Risk tolerance at the time of authorization

Why it matters: Two identical payments may receive two different outcomes depending on context. This is where intelligence — not brute-force retries — matters.

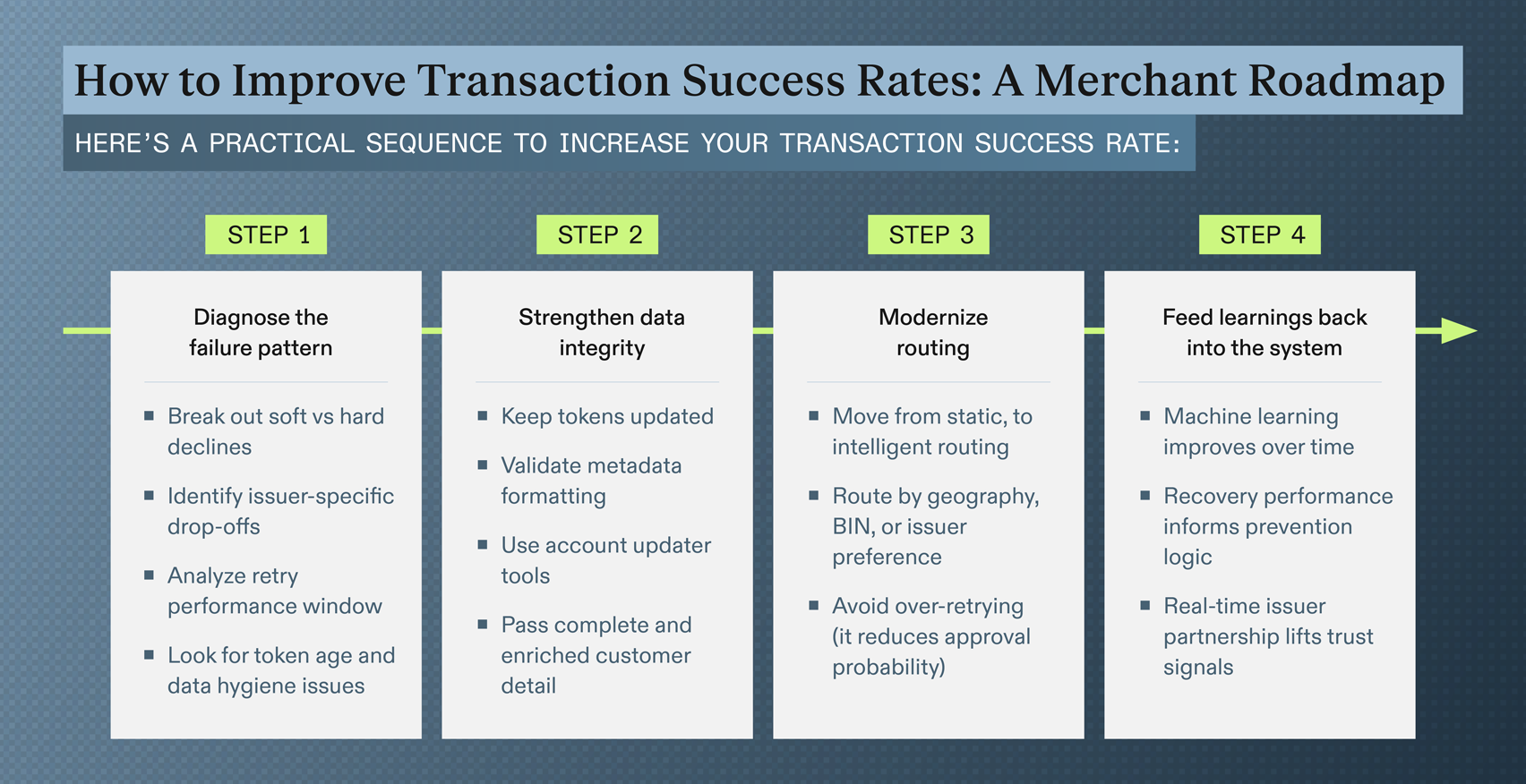

Data Is the Currency of Approval

When people ask how to improve transaction success rates, we start with data because issuers make authorization decisions based on what they see. Think of metadata as your side of the conversation sharing what the bank needs to see. The more details you provide, the more confidently a bank can approve a transaction.

Strong data signals include:

- Fresh network tokens

- Accurate customer identity fields

- Up-to-date billing information

- Purchase history & behavioral continuity

- Token refresh and lifecycle management

Why it matters: Data quality is one of the fastest ways to improve transaction success rate without touching acquisition or price.

How Routing Influences Transaction Outcomes

Routing is the payments world’s version of traffic control. The same payment, sent through a different path, can yield a different outcome.

Optimization opportunities:

- Gateway prioritization by geography

- Routing at BIN or issuer level

- Smart retry rules informed by decline reason

- Avoiding repeated attempts that weaken approval odds

- Leveraging tokens and network-level insights

Why it matters: In many cases, the same transaction sent through a different gateway, network token, or routing path can flip a decline into an approval — without changing the customer experience at all.

What Happens Inside Issuer Logic?

On the other side of every payment is an issuer making areal-time decision to approve or decline the transaction. That decision is based on a mix of factors, including the perceived risk versus legitimacy of the payment, the customer’s available balance and credit limits, the likelihood of fraud, the merchant’s trust profile, and historical approval patterns. The simple truth is that success doesn’t come from trying to outsmart issuer logic—it comes from aligning with it.

Where Legacy Recovery Falls Short

Recovery is important, but it’s fundamentally reactive — it helps you win back what’s already been lost. To truly improve transaction success rates, the real gains come from preventing failures upstream rather than chasing them downstream. This is where Revaly’s philosophy moves the industry forward. By combining prevention, intelligence, smart routing, and stronger issuer alignment, we reduce declines at the source and elevate transaction success rates before recovery is even needed.

The Revaly Approach

By now, one thing should be clear: transaction success rate isn't something you "optimize" with a single fix. It’s the outcome of an interconnected system where data quality, routing decisions, timing, and issuer trust all compound to determine whether a legitimate payment is approved or declined.

Most payment stacks weren't designed with this system in mind. They treat failures as downstream problems, rely on static rules, and attempt to recover revenue only after trust has already been eroded with the issuer and the customer.

Revaly was built around a different premise: If you want higher transaction success rates, you have to design for approval, not react to decline.

That means shifting from fragmented tools to a coordinated approach that:

- Improves how transactions are presented to issuers

- Chooses how and where payments are routed based on real performance signals

- Adjusts behaviour based on issuer response, not assumptions

- Learns continuously from every attempt, success, and failure

The outcome? More approvals, more renewals and more revenue without more marketing spend.

Final Thoughts

Transaction success rate reflects how well a payment system converts real customer intent into approved transactions When data is clean, routing is smart, and issuer logic is understood, transaction success becomes the norm instead of a fortunate outcome. Because most merchants don’t need more traffic—they need more successful payments from the customers who are ready to buy.

Want to improve your transaction success rate? Talk to our team or explore how Revaly helps merchants engineer approvals instead of chasing losses.